Budgeting for Salaries is Key to the Nonprofit Budget Building Process

This piece is Part 3 of 4 in our Budget Building Essentials Series.

When preparing a nonprofit organization expense budget, I generally favor using a programs and operations approach rather than an expense by line-item method. The one exception is budgeting for staff costs (salaries, employee benefits, and payroll taxes), which is usually the largest expense line-item in a nonprofit’s budget. Preparing a separate labor budget at the front end of the budget building process will enhance planning and improve management of the organization’s workforce.

There are advantages to preparing a separate labor budget isolated from the rest of the budget building process. The advantages include providing an effective early starting point for the budget building process, addressing workforce capacity, resource allocation, and performance issues, and safeguarding confidentiality.

Getting off to an effective early start on the annual budget building process is a must. One of the best tactics is to assemble a first draft of the labor budget at the front end of the budget building process. After assessing nonprofit organization revenue and funding resources, labor is always a close second variable in evaluating organizational and operational capacity constraints. Consequently, having an early picture of the workforce that includes changing personnel, salaries, and other compensation-related cost factors will help set the stage for building a realistic and achievable budget for the next fiscal year.

Before getting too deep into the budget preparation process, it is best to first address workforce (labor) capacity, resource allocation, and performance issues instead of just focusing on programming and operational objectives and hoping there is the right-skilled staff, with appropriate salaries, to meet organizational needs.

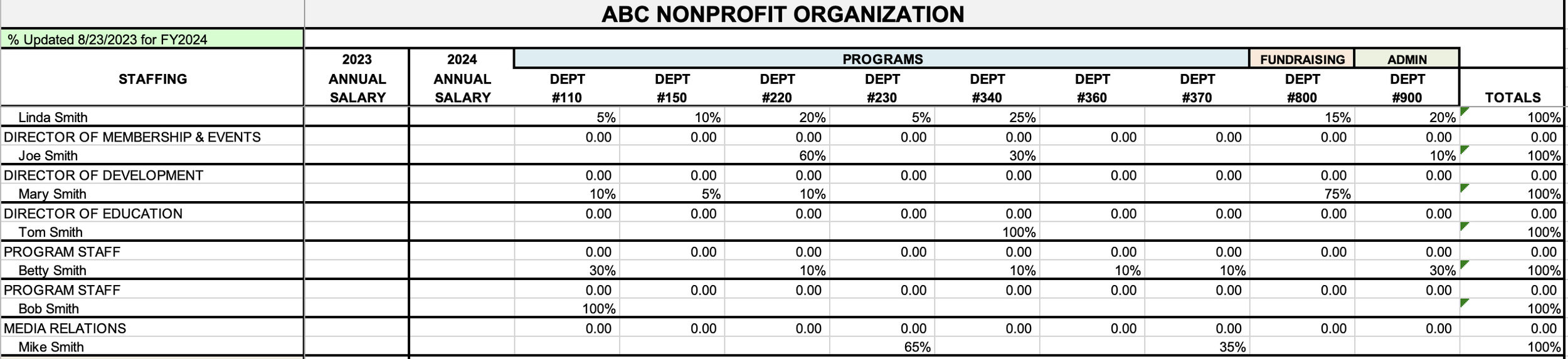

Begin by setting up a master labor budget worksheet organized by individual staff positions (vertical rows) with columns for current salaries followed by columns for labor effort allocations for programs, fundraising, and administrative (overhead) departments.

The labor budget worksheet will allow you to view individual salaries as well as the total organization cost of salaries. The worksheet will also show how compensation costs are expected to be divided (allocated) to programs, fundraising, and administrative (overhead) departments. This is key to computing and understanding the full cost of programs, fundraising, and administration while helping to comply with generally accepted accounting principles (GAAP) financial statement presentation requirements and IRS Form 990 reporting of expenses.

The labor budget worksheet will not only show total compensation costs, it will also display how staff is planning to allocate their time and efforts. This is accomplished by assigning time and effort percentages to areas of responsibility for each staff position. Even small changes to staff time and effort allocations can have a big impact on program effectiveness and the organization’s bottom line.

The front end of the budget building process is also the best time to consider changes to job descriptions, redirection of time and effort allocations, and other staffing changes. Getting started early with this process will enhance program planning by helping you to better align the organization’s workforce to meet mission goals and improve the performance of individual employees as well as the organization as a whole.

The following labor budget worksheet example is provided for demonstration purposes. Notice the percentage of time and effort allocations and how they are separate from the salary column.

(a labor budget worksheet template consistent with this example can be downloaded in excel format here)

From this labor budget worksheet, a clear picture of salary cost and assigned responsibility areas can be seen. Capacity and expected labor allocations, along with individual and operational performance, can be easily assessed and repositioned.

How can the organization safeguard confidentiality of individual salaries? Simple, just erase the salaries in the first two columns and what is left is time and effort allocations.

(a labor budget worksheet template consistent with this example can be downloaded in excel format here)

The worksheet without salaries can be shared with management and staff for reviewing time and effort allocations, encouraging discussion about how modifying staff responsibilities could impact future operations and address potential capacity issues.

Finally, after time and effort allocations are adjusted, salaries are repopulated back into the worksheet. Now the bottom portion of the worksheet can be returned to the staff so they can add salary and related payroll taxes and employee benefits expenses into their program budgets without consequences from individual salary information being exposed.

(a labor budget worksheet template consistent with this example can be downloaded in excel format here)

Planning Tip – One roadblock to setting the salary budget for the next fiscal year is addressing how future potential salary increases for cost-of-living, performance, and promotions will be distributed. This can be rectified by including only current salaries by position and adding a separate total line for salary increases, raises, bonuses, and such that will be applied by senior management discretion during the next fiscal year.

There are so many factors to consider when budgeting for employee salaries and other related compensation costs. Front-ending the budget building process around the labor budget will provide extra time to game-plan, implement staff training and development programs, and determine whether to make other changes such as adding new positions, modifying job responsibilities, promoting or replacing some current staff, and perhaps even implementing a reduction-in-force for operational areas that are no longer needed due to evolving conditions.

All these changes take time. The opportunity costs of delaying this planning can be high and potentially damaging.